1. Start by Examining the Work Itself

Before you look at any price database, spend time with the artwork. Document everything you can observe:

- Dimensions — measure height, width, and depth precisely

- Medium and materials — oil on canvas, watercolor on paper, bronze, photograph, print, etc.

- Signature, date, and edition number — look front and back

- Condition — note any damage, discoloration, repairs, or sun fading

These details directly affect value. A signed, well-preserved original in a desirable medium will almost always command a higher price than an unsigned print with condition issues.

2. Research the Artist

Context matters enormously. An artwork's value is inseparable from the artist's career trajectory. Look into:

- Exhibition history — has the artist shown in major galleries or museums?

- Representation — are they carried by established dealers?

- Publications and press — critical recognition strengthens value

- Career stage — when in their career was this piece made?

Free resources for artist research include the Getty Research Institute, RKD Artists, and Artprice (free biographies and signatures).

Dealers play a significant role in building an artist's market value. As Rose Fredrick writes, strong gallery representation—exhibitions, press, museum placement—often signals a healthy, growing career. If museums are collecting the artist's work, consider that a meaningful endorsement.

3. Find Comparable Sales

The most reliable way to establish a price range is to find what similar works by the same artist have sold for recently. This is called the comparable market data approach, and it's what most appraisers rely on.

Key factors for finding good comparables:

- Same medium — paintings trade differently than prints or works on paper

- Similar size — larger works generally fetch higher prices

- Same period — an artist's early work may value very differently from their mature output

- Recent sale date — comparables older than five years may not reflect today's market

Useful databases for auction results include Artnet Price Database, Artprice, and MutualArt. Some offer limited free access; subscriptions unlock advanced filtering by medium, size, and date.

4. Understand What Drives Price Up (and Down)

Two seemingly identical works by the same artist can sell for wildly different amounts. The gap usually comes down to a handful of factors:

Increases Value

- → Strong provenance (notable previous owners)

- → Inclusion in a catalogue raisonné

- → Recent exhibition or publication

- → Rarity — few works from that period on the market

- → "Fresh to market" — first time at auction

- → Excellent condition

Decreases Value

- → Damage, heavy restoration, or fading

- → Uncertain or incomplete provenance

- → "Bought-in" — failed to sell at a previous auction

- → Over-supply — too many works by the artist on the market

- → Falling out of fashion in the current market

- → Subject matter that's less desirable within the artist's body of work

Subject matter can be surprisingly influential. As Artnet notes, Impressionist still lifes trade in a slightly different market than landscapes or portraits by the same artist. Similarly, a Picasso from his rare Blue Period commands far more than a figurative work from the 1950s.

5. Know the Three Types of Valuation

Not all valuations are the same. The number you need depends on why you need it. The three most common types:

Fair Market Value (FMV)

The price a work would sell for between a willing buyer and willing seller, neither under pressure. Used for estate planning, tax reporting, charitable donations, and family division. The American Society of Appraisers defines this as the standard for most legal and tax-related purposes.

Retail Replacement Value

What it would cost to replace the work with something of similar kind and quality within a reasonable timeframe. This is typically the highest valuation and is what insurance companies use. It includes sales tax, import duties, and any commissions.

Market Value (Marketable Cash Value)

Fair market value minus selling costs (auction fees, dealer commissions). Used in divorce settlements, partnership dissolutions, and scenarios where the goal is to determine net proceeds from a sale.

Getting the wrong type of valuation for your situation can be costly. Don't give your estate planner a retail replacement number, and don't insure your collection at fair market value.

6. When to Hire a Professional Appraiser

For high-value works, legal matters, or insurance claims, you'll need a qualified appraiser—not just an opinion from a dealer or friend. Look for appraisers who follow USPAP standards (Uniform Standards of Professional Appraisal Practice).

Find accredited appraisers through:

Choose an appraiser who specializes in the type of art you own and has no conflict of interest—ideally someone who doesn't also sell art. As the Winston Art Group advises, review valuations annually. Markets shift, and your insurance and estate plans should reflect current reality.

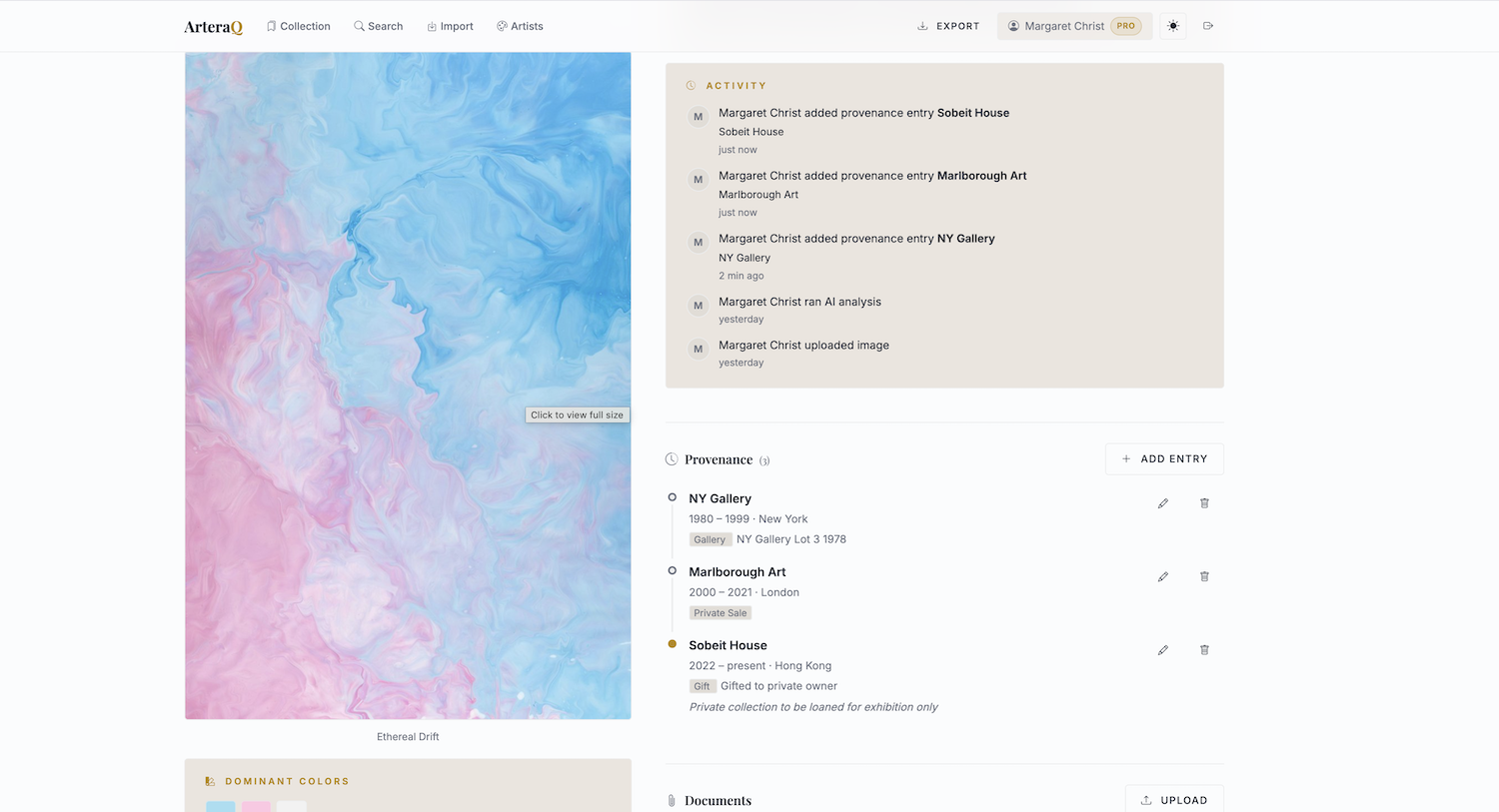

7. The Role of Provenance

Provenance—the documented history of an artwork's ownership—is one of the strongest factors in determining value. A clear chain from the artist's studio through reputable dealers and collections adds credibility, while gaps raise questions about authenticity and can significantly reduce value. Works owned by notable collectors, exhibited in museums, or published in catalogues raisonnés consistently achieve higher prices.

Keep thorough records of every acquisition: who you bought from, when, how much you paid, and any supporting documentation. This is exactly where ArteraQ excels—its built-in provenance tracking lets you document every ownership transfer in a structured timeline, complete with attached invoices, certificates of authenticity, and gallery receipts, giving you a clean, verifiable chain of custody that strengthens your artwork's value.

8. Track Your Collection's Value Over Time

Valuation isn't a one-time event. Markets change, artists' reputations grow (or fade), and your collection evolves. Best practices:

- Review values annually — even a quick check ensures your insurance and estate plan stay current.

- Record purchase price and current valuation side by side — this shows growth and helps with decision-making.

- Store appraisals digitally — attach them to each artwork record so you can reference or share them instantly.

- Export reports for insurance renewals — your insurer will appreciate organized, up-to-date documentation.

A dedicated art inventory tool makes this dramatically easier than spreadsheets. ArteraQ, for example, lets you track purchase price, fair market value, and insurance value per artwork—and export collection reports when you need them.

9. Common Mistakes to Avoid

Even experienced collectors make valuation errors. Watch out for these:

- Confusing purchase price with current value — what you paid years ago may have nothing to do with what it's worth today.

- Using the wrong valuation type — insurance value ≠ estate value ≠ resale value.

- Relying on a single comparable — one auction result isn't a market; look for patterns across multiple sales.

- Ignoring condition — damage, restoration, and fading can reduce value by 30–50% or more.

- Skipping documentation — without records, proving provenance and value becomes much harder.

10. A Simple Valuation Framework

You don't need to be a market expert. For most collectors, this practical framework works well:

- 1. Examine the work — medium, dimensions, condition, signature

- 2. Research the artist — career, exhibitions, representation

- 3. Search for comparables — same medium, similar size, recent sales

- 4. Consider provenance and rarity — documented history adds value

- 5. Determine which valuation type you need — FMV, replacement, or market

- 6. For high-value works, hire a USPAP-compliant appraiser

- 7. Record everything — and review annually